Kambi: This stock is a long term investment candidate

Analysis published on Aug 9 2020. Last Traded Price 217.40 SEK / share

Summary:Kambi provides the leading independent sportsbook platform in a PaaS (Platform-as-a-Service) model to online sports betting companies (operators). In Jul 2020, Kambi received EGR B2B Awards for both Sportsbook Platform Provider and Sports Betting Supplier of the year

With legalization of sports betting in US kicked off on a state-by-state basis since 2018, multiple operators in US have already selected Kambi as its platform of choice for sportsbook. With its high-quality solution and several reference operators in US, Kambi holds the leadership position to get adopted by significant number of sports betting operators in US

COVID-19 is accelerating the pace of launch of online sports betting. With global sports starting up slowly during 2020, online/kiosks based/BYOD (bring your own device) on-premise sports betting have bright future ahead

With significant market opportunities in both near term and long term, low correlation to the stock market index in prevailing highly uncertain market conditions and being an independent sportsbook platform provider with strong economic moat; Kambi is a good addition to an investment portfolio with a strong growth potential

Welcome, Reader. In this article, I am sharing my personal analysis on Kambi as a long-term investment candidate.

Step 1: Let’s first understand Kambi’s industry, business and its economic moat

Sports Betting Industry

Sports Betting industry is getting increasingly legalized with countries realizing the potential to generate tax revenues which are otherwise getting lost due to the absence of legalized sports betting. Sports betting has been made legal in US in 2018 after the US Supreme Court struck down the PASPA (Professional and Amateur Sports Protection Act) in 2018. However, the regulatory regimes for sports betting are highly fragmented varying by every country (even varying between states of US) - which makes it difficult for the companies operating in the industry, and are exposed to high regulatory risks.

Kambi’s positioning in the Sports Betting Industry

Kambi, with headquarters in Malta, Europe, came into existence in 2010 when Kindred (earlier Unibet) spun-off its sports betting B2B business into Kambi Sports Solutions. Backed by an experienced management team, strong execution and consistent performance since inception, Kambi was named among Europe’s fastest growing companies in the Financial Times 1000 list in 2017. In 2018, Kambi created history by becoming the first sportsbook to process the first legal wager in New Jersey, post-PASPA.

Source: Kambi’s website

Information Providers (Suppliers to Kambi) provide (near) real-time updates of live events to enable Kambi to provide odds for the events to its operators.

B2C Operators (Customers of Kambi) provide player (consumer) facing application for the players to wager.

End Users (Players) are individuals who wager/place their bets with the B2C Operators.

Kambi’s solution to its Operators includes a broad offering of front-end user interface for players, odds compiling engine, customer intelligence and risk management, built on an in-house developed software platform.

As of Jul 2020, Kambi’s 20-plus customers included 888 Holdings, ATG, DraftKings, Greenwood Gaming & Entertainment, Kindred Group, LeoVegas, Mohegan Gaming & Entertainment, Penn National Gaming, Rank Group and Rush Street Interactive. Kambi employed more than 850 staff across offices in Malta (headquarters), Australia, Romania, the UK, Philippines, Sweden, Australia and the United States.

Competitors for Kambi

Inhouse sportbook service of operators - they would have that operator as its captive customer and (most likely) only customer, however they would lack the benefits of economies of scale, R&D investment/innovation intensity

Sportsbook providers like OpenBet, IGT

Kambi’s Revenue Model with Operators:

Monthly/annual fixed Subscription Fee

90% of revenues as Revenue Share - a percentage of Operator’s Net Gaming Revenues (NGR = Gross Gaming Revenues or GGR for operators from the bets placed by their players/users adjusted for various items like promotion costs, decided on an individual contract basis)

The Revenue Model thus motivates Kambi to provide odds that maximizes the operators’ NGR, thereby aligning Kambi and its operators’ interests.

Kambi’s Scalable business: Kambi’s cost does not scale with increase in number of players/users for its operators (thus increase in NGR for operators). Kambi incurs high fixed cost for its technology infrastructure (to provide a premium service and experience: receiving real-time updates from its information providers, processing those and providing real-time odds for its operators) and relatively low variable cost (when onboarding additional operators on the existing infrastructure). The effort towards operating any live event does not change due to the number of players/users.

Experienced Management team of Kambi: Kambi’s CEO (Kristen Nylen), Deputy-CEO (Erik Lögdberg, leading product and operations), CFO (David Kenyon) have been with the company since the Unibet-era (prior to 2010) and amongst themselves, hold 880K+ shares and 300K+ options of Kambi’s stock. They have proven themselves by delivering consistent performance of Kambi and they own considerable equity in the company.

Strong Economic Moat for Kambi:

Platform-as-a-Service (PaaS) offering that enable its customers (operators) to provide differentiated and exciting sports betting player experience to its users, through the platform that includes a layer of operator empowerment around the high-performance Sportsbook engine core. The PaaS offering also enables Kambi to achieve high margins in its business, roll-out technical improvements and/or innovations faster to its existing operators, and also enable new operators to get onboarded and roll-out its offering to its market faster.

Scalability of Revenues and Profitability: 90% of Kambi’s revenues are based on revenue sharing model with its operators - so, as long as sports betting continue to grow, Kambi’s scalable business continue to grow with increasing profitability (as costs are not directly linked to revenues).

20+ operator customers whose business would be severely affected without Kambi and would have incur significantly high switching cost and complexity to change its sportsbook platform.

Step 2: How has Kambi’s stock performed till date?

As 90% of Kambi’s revenues is based on Revenue Share with its operators (customers), Kambi has created a “Kambi Turnover Index” which captures its operators’ turnover. The chart below illustrates Kambi’s operators’ quarterly turnover and betting margin. The operator turnover of the first quarter of 2014 was indexed at 100. The operator trading margin is shown on the right-hand axis. The index changes as Kambi acquires new customers (operators) and/or when the turnover of the operators changes. The turnover and margins of the operators are impacted by the outcome of sporting events.

Kambi aims to achieve optimal margin, to maximise turnover growth and boost the financial performance of its operators (customers) – both in the short and long term. Kambi manages this by leveraging its risk management tools.

Looking again into the chart below, we see that the Turnover Index has a growth trend, with occassional dips (like Q2 2020 as multiple sport events did not happen due to COVID-19).

Source: Kambi’s website

However, if I look into individual month in Q2, we see June 2020 performance (of operator turnover) bit higher than that of June 2019.

Source: Kambi’s website

Even during the tough quarter of Q2, Kambi managed to increased its Cash position slightly, to keep it at the level of 46+Million EUR.

Source: Kambi’s website

Kambi’s revenues have historically been dependent upon the European market. Since 2018, with legalization of sports betting in US, increasing contributions from the emerging US market is observed and expected to increase exponentially within the next 3 years. In addition, Kambi has achieved success with Central and South American operators - which is poised for significant growth over the next 3 years. There has been dip for Q2 as multiple sport events did not happen due to COVID-19. Below chart shows the geographical spread Kambi’s operators’ GGR (Gross Gaming Revenue) over the recent quarters. When I look further, my view is that Europe and Americas would roughly be the equal size for Kambi in three years timeframe.

Source: Kambi’s website

Now, let’s look into Kambi’s EPS (Earnings per share) performance over the past three years. I find that Kambi has consistently performed in delivering positive EPS, which have been also above forecast (barring Q1 2017 and Q2 2020).

Source: Investing.com. EPS in USD/share

Another I like to look into, more so during present uncertain times - is a company’s Long-Term Debt to Equity ratio/percentage. I prefer it to be 0.25/25% or less, to support the company in riding out the uncertainty. For Kambi, its Long-Term Debt ratio is less than 0.2/20%.

How has Kambi’s stock performed?

The chart below shows Kambi’s stock performance and compared with OMX Stockholm 30 index over the past three years. The stock performance provides a good view on how well the stock has out performed the index during that period.

Source: Avanza

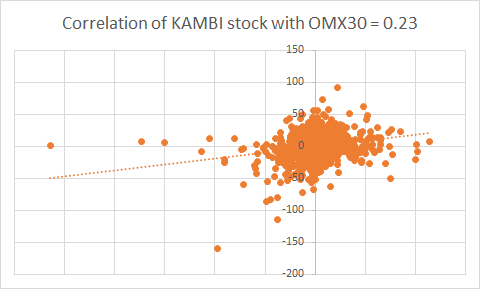

In addition to past performance, another metric I like to consider when evaluating any stock for my portfolio - is the stock’s correlation to the index. To combine with stocks highly correlated to the index (like banking, manufacturing stocks), as a diversification measure, it is important to add stocks which have low correlation to the index.

Correlation of Kambi’s stock with OMX30 index over past years is a low 0.23. I like it, from a portfolio diversification perspective.

Step 3: What may be the future growth potential for Kambi?

Let’s first find out the growth potential for the online sports betting business.

As per the chart below, online betting is largest contributor to online gambling and poised to grow the fastest - with global operator GGR growing from roughly 25B EUR to 35B EUR in the next 3 years.

The below charts show the operator GGR growth expected across Europe and Brazil (the most important market in Latin America).

US sports betting market is poised to explode, with more states legalizing sports betting to increase its tax revenues given the negative impact on its revenues due to COVID-19. There are reports on the internet which state the range of USD 5 to 8 Billion as the US sports betting market size by 2025, from the size of approx. USD 800Million in 2019 (more information can be found at Legalsportsreport.com) . In the chart below, the states in dark blue plus Colorado are the states wherein operators have already selected Kambi’s platform. Growth in GGR for operators in such states plus additional GGR through operators in more states legalizing sports betting selecting Kambi, presents the significant opportunity for Kambi in US.

Source: Kambi’s website. In addition, Colorado legalized sports betting in Nov 2019, and Kambi has gone live with Rush Street and DraftKings in May 2020

The Native American gaming opportunity in the US is another significant one. The Native American tribal governments operate gambling enterprises on a reservation or other tribal lands. These are not regulated by state laws and are governed by the Indian Gaming Regulatory Act of 1988. There are approximately 500 gaming operations across 29 states run by more than 240 tribes, with total annual revenue of approx. USD 30bn. Sports betting is an increasing interest area for these gaming operations as well. Kambi has already partnered with two well respected tribal owned gaming companies: Mohegan Gaming & Entertainment (MGE) and Seneca Gaming. Kambi has the potential to be the leading supplier to this market as well.

Source: Kambi’s website.

Listing of Kambi in US stock market - Given the inroads Kambi has already made in US, the future growth potential that clearly exists in US, US markets being flush with liquidity presently and to increase efforts to reduce the percentage share of maturing Europe business, if I were in Kambi’s management/board, I would be actively considering listing in US. During the COVID-19 impact period (April to May 2020), DraftKings (an operator and one of Kambi’s customer) and GAN Limited (a gaming software provider) achieved successful listing in US stock markets.

Overall, from a potential perspective, Kambi as the leading high-quality scalable sportsbook provider is in the pole position to benefit from the increasing legalized sports betting globally, and more specifically in US and Brazil.

Step 4: Why have I invested in Kambi for my long-term investment portfolio?

Legalized Sports betting industry holds significant growth potential in the next three to five years. This industry has shown its resilience during the COVID-19 impact period of March to June 2020

Kambi’s strong economic moat and its execution experience and capabilities would enable it to maintain its leadership position in the industry and take a large pie of the growth in the legalized sports betting industry

Kambi also possesses a low debt / equity ratio, healthy cash levels, historical healthy cash flow from operations, low correlation to the index

Possible and probable listing in US - this could become a watershed moment for Kambi’s stock

Step 5: Let’s apply Negative Reverse - why should one sell Kambi’s stock?

Buyers and sellers co-exist and need each other for a liquid market.

I like to do negative reverse of my analysis to understand the counter opinions, find holes in my thinking and go about finding answers to those.

So, let us do a negative reverse - “why should one sell / not buy Kambi stock right now?!”

COVID-19 impact is going to continue across the world, which would not let sports event to happen (at the similar levels of pre COVID-19) in the foreseeable future. So, it is better to wait and watch before committing to buy into Kambi, or for that matter, any stock related to sports events

Sports betting industry is exposed to highly fragmented regulatory risks, thereby bringing in uncertainties for a global provider like Kambi

Kambi’s stock has already achieved significant growth since March 2020 and future growth expectation for next 2-3 years are already priced in the present price levels

Kambi’s stock has high PE levels of 40-50, which makes the stock an expensive one to purchase

Call to action for you: Will you make a long term investment in Kambi?

Additional articles you may read: